Investment Insight: PT Cita Mineral Investindo Tbk (CITA) – Beyond Bauxite Mining

Executive Summary

As global aluminum prices reached a 4-year high in January 2026, CITA is positioned as a unique play in the metals sector. While often categorized solely as an upstream bauxite miner, CITA’s true profitability is now driven by its downstream "money machines" through associate entities (WHW and KAI), rather than just raw ore sales.

1. Market Context: The Aluminum Bull Run (H2 2025 – Jan 2026)

The aluminum market has experienced significant structural tightness over the last six months:

- Price Surge: Since mid-2025, aluminum prices have steadily climbed from approximately USD 2,500/MT to peaks near USD 3,300/MT in January 2026.

- Supply Scarcity: Bullish scenarios predicted by analysts have materialized due to structural tightness in the global market.

- Demand Drivers: Increased demand from the electric vehicle (EV) sector and solar panel manufacturing has created a persistent deficit, keeping prices elevated.

Impact on CITA: This macro trend directly enhances the valuation of CITA’s downstream assets, particularly its stake in the aluminum smelter (KAI) which is expected to produce 500,000 tons of aluminum per year starting in 2026.

2. Deep Dive & Narrative Correction: Fact vs. "Rough Calculation"

While the presentation slides offer an optimistic outlook, a professional investor must distinguish between theoretical potential and financial reality.

A. The "Gross Value" Illusion

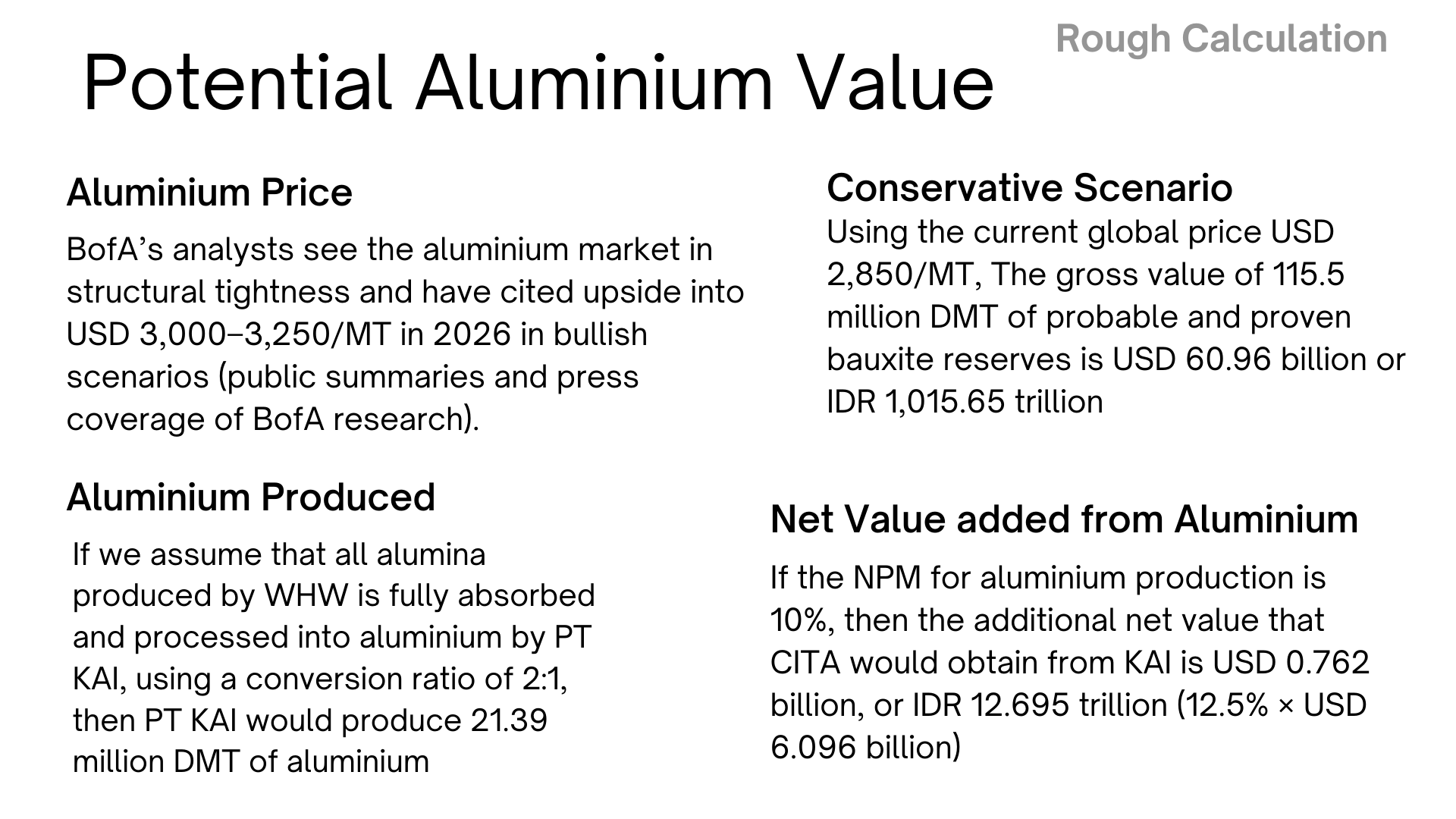

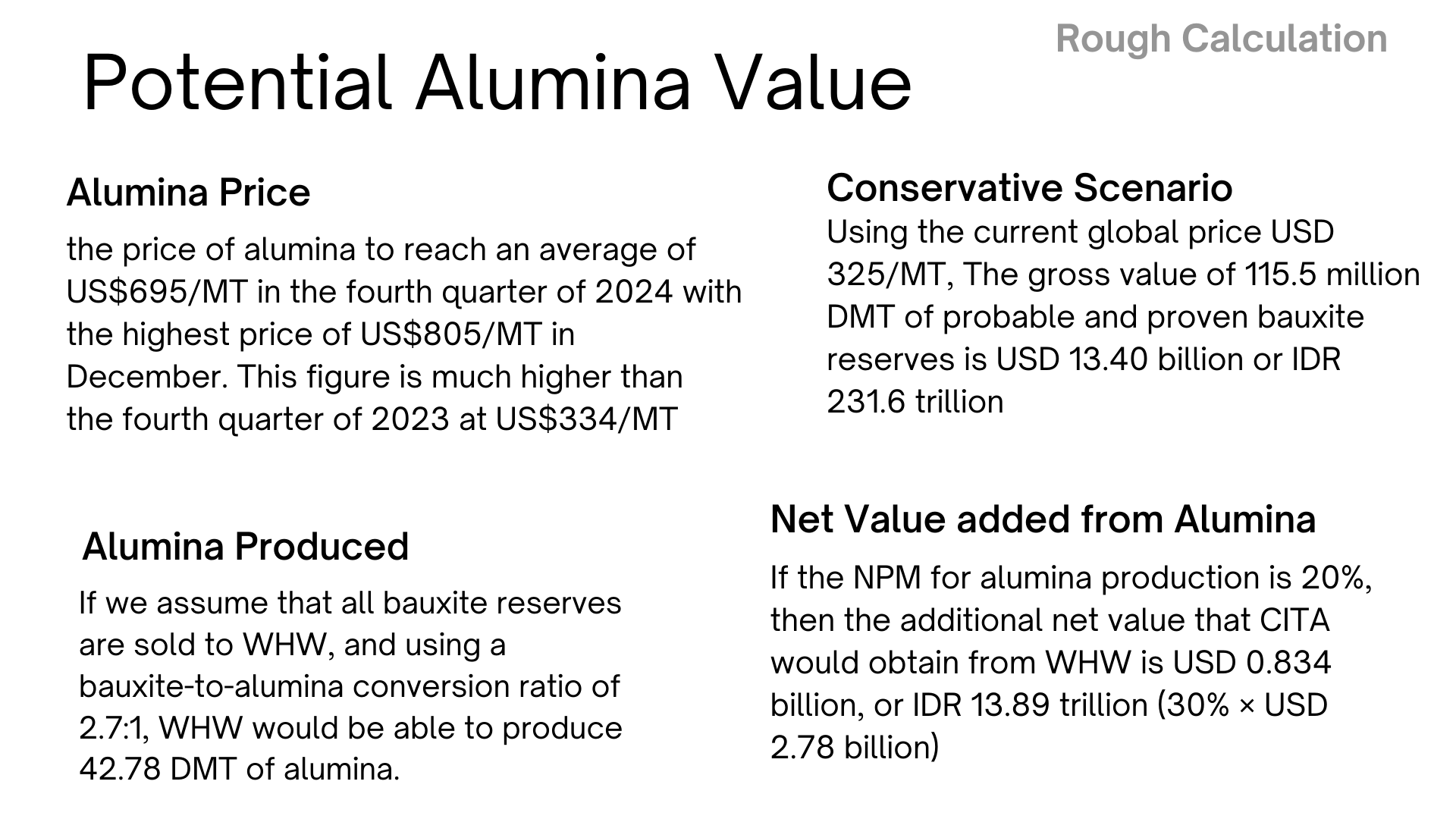

Slide Analysis: The slides present a "Potential Value" of up to USD 60.96 billion (over IDR 1,000 trillion) based on total bauxite reserves.

Correction: It is critical not to confuse "Gross Value" with Company Valuation. A mining company is never valued based on the total theoretical sales price of its ground reserves, but rather on its annual Cash Flow and monetizing capability.

The Reality: The IDR 1,000 trillion figure is a theoretical maximum revenue over decades. The real focus should be on the "Current Net Profit," which soared by 246% to IDR 2.49 trillion despite a slight decline in production and sales volume.

B. The Value of Downstream Associates

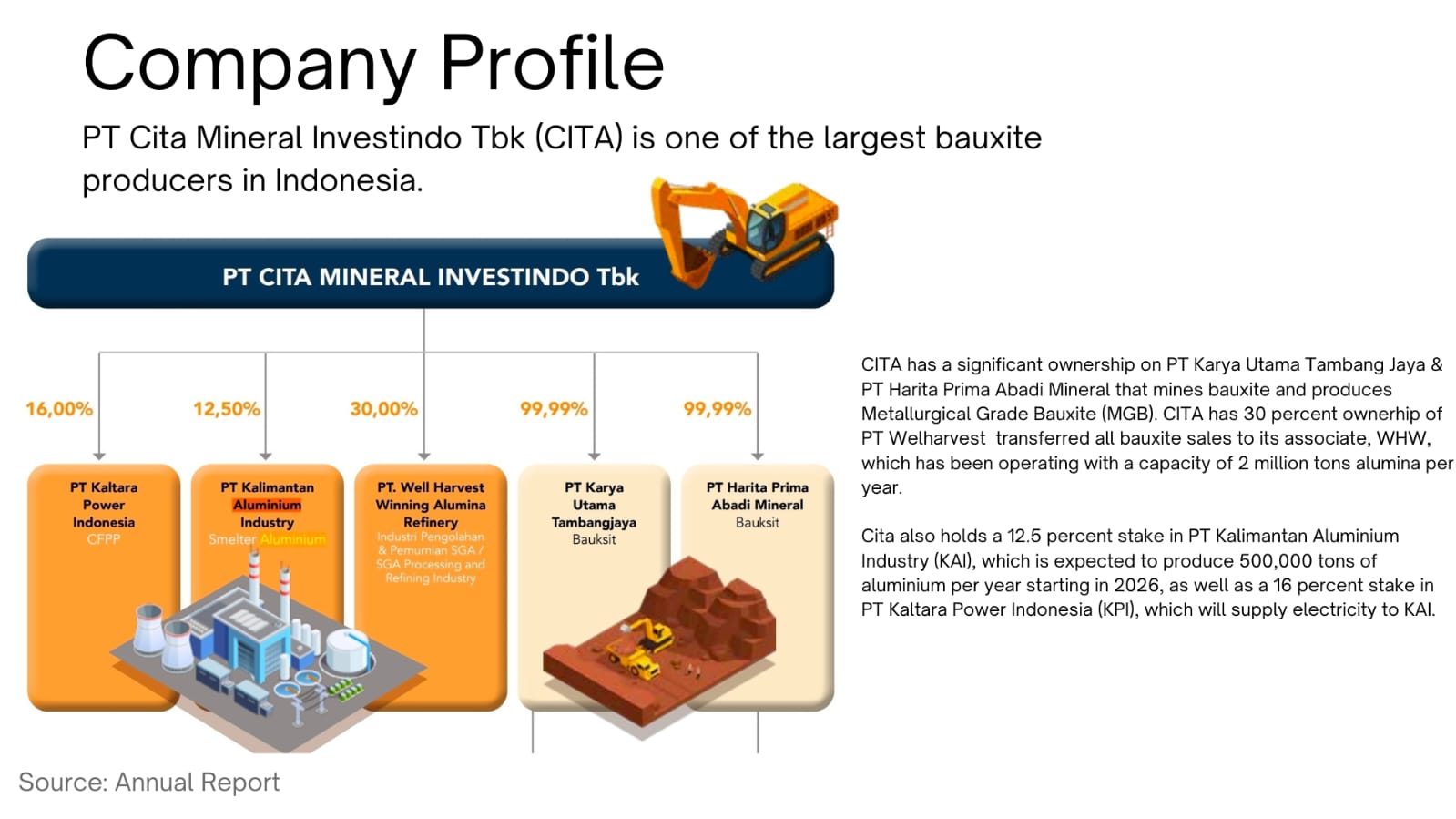

CITA’s intrinsic value lies in its strategic ownership of downstream facilities:

- Alumina (WHW – 30% stake): This refinery has been operating with a capacity of 2 million tons of alumina per year. It serves as a primary "cash cow," with CITA benefiting from the net profit of this associate rather than direct operations.

- Aluminium (KAI – 12.5% stake): With production starting in 2026, this is the next major growth catalyst. At current aluminum prices above USD 3,000/MT, smelter margins are significantly thicker than those of raw bauxite or alumina.

3. Valuation Summary & Strategy

Based on the current data (Market Cap IDR 16.356 trillion, PER 5.50x, PBV 1.95x):

- Current Status: CITA appears undervalued relative to its growth trajectory. A Price-to-Earnings (PER) ratio of 5.50x is exceptionally low for a company recording triple-digit profit growth (246%).

- Upside Potential: The market has likely not fully "priced in" the contributions from the KAI aluminum smelter.

- Risks to Watch: Potential negatives include unstable operating cash flow and oversupply in the broader commodity market leading to falling prices.

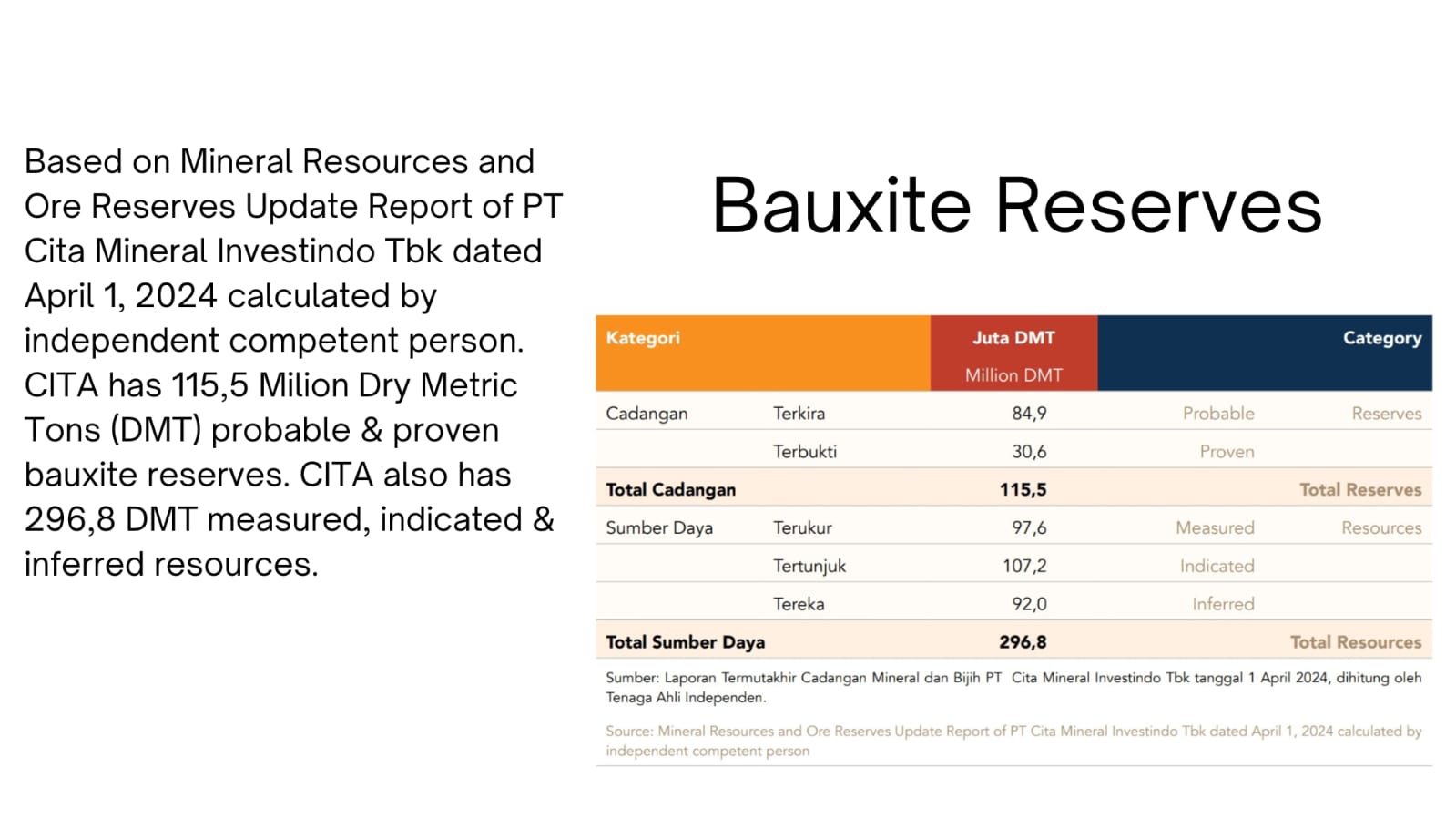

Bottom Line: CITA should be viewed as the most affordable proxy for downstream aluminum and alumina refining in Indonesia. Its value is anchored by the 115.5 million DMT of probable and proven bauxite reserves which provide the essential feedstock for its high-margin downstream associates.

This reflects my personal investment decision and perspective. It is not intended as investment advice or a recommendation to buy, sell, or hold any securities. Investing in the capital market involves significant risks, including the potential loss of capital. Each investor should conduct their own research and make decisions according to their individual risk tolerance and financial circumstances.