Why Pakuwon Jati (PWON) Remains a Top-Tier Resilient Property Stock

PT Pakuwon Jati Tbk (PWON) stands out as one of the most structurally defensive property developers in Indonesia. Its business model—emphasizing high recurring income, conservative financial management, and disciplined expansion—differentiates PWON from its cyclical peers and underpins its long-term investment appeal.

1. Strong Cash Flow Stability Driven by Growing Recurring Income

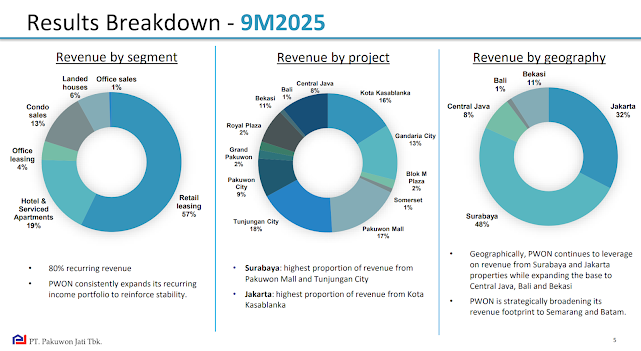

PWON is widely recognized as the leader in recurring income within the Indonesian property sector. With a portfolio of "Superblocks" that integrate shopping malls, hotels, and offices, approximately 70%–75% of its total revenue is derived from recurring sources. This provides a massive cushion against the volatility of the residential pre-sales (marketing sales) market.

2. Industry-Leading Profitability and Operational Efficiency

PWON consistently records one of the highest net profit margins in the sector, often exceeding 30%–40%. This reflects superior operational efficiency and the premium nature of its assets, such as Gandaria City and Kota Kasablanka. Its "land bank" was largely acquired at low costs years ago, allowing for high-margin developments today.

3. Strategic Focus on Hospitality and Retail Post-Pandemic

Recognizing the structural shift in the office market—where oversupply and remote work have slowed growth—PWON has pivoted toward the hospitality and retail sectors. The recovery in tourism and domestic consumption has led to record-breaking mall traffic and high hotel occupancy rates, effectively offsetting the stagnation in office space demand.

4. Attractive Valuation with a Margin of Safety

Despite its superior balance sheet and dominant market position, PWON often trades at a significant discount to its Net Asset Value (NAV). Compared to historical averages, its current P/E and P/BV multiples offer an attractive entry point for value investors looking for a "Blue Chip" property stock at a reasonable price.

5. Steady Earnings Recovery Towards Pre-Pandemic Levels

While net profit peaked in 2019 due to one-off gains and a booming residential market, PWON has demonstrated a consistent upward trajectory in core earnings since 2021. The recovery is driven by organic growth in rental rates and the full-year contribution of newly acquired assets, signaling a return to its long-term growth trend.

6. Disciplined Expansion in High-Growth Regions

PWON pursues a "measured expansion" strategy, replicating its successful mixed-use model in new territories. Key growth catalysts include:

- IKN (Nusantara): Development of the Pakuwon Nusantara mixed-use complex.

- Semarang & Batam: New mall and hotel projects are currently under development to capture regional purchasing power.

7. Fortified Balance Sheet and Conservative Leverage

PWON maintains one of the healthiest balance sheets in the industry, characterized by a low Net Debt-to-Equity ratio. Its management prioritizes liquidity, ensuring the company can meet its USD-denominated bond obligations while maintaining enough "dry powder" for opportunistic investments.

8. Strategic Resilience and Opportunistic Acquisitions (2020–2023)

During the COVID-19 crisis—a period when many property developers faced severe liquidity pressure—PWON demonstrated exceptional financial strength by executing a series of high-profile, opportunistic acquisitions. Leveraging its robust cash reserves, the company strategically expanded its portfolio in Central Java and Bali.

In November 2020, PWON finalized a major IDR 1.36 trillion acquisition of assets from the Duniatex Group, which included Hartono Mall Yogyakarta (now Pakuwon Mall Jogja), Hartono Lifestyle Mall Solo Baru (now Pakuwon Mall Solo Baru), and the Yogyakarta Marriott Hotel. Following this, in March 2023, the company further expanded its hospitality footprint by acquiring the Four Points by Sheraton Bali, Kuta, for IDR 165 billion. These acquisitions, funded primarily through internal cash, allow PWON to capitalize on the resurgence of tourism and regional retail growth without overleveraging its balance sheet.

Company Update September 2025 - PT Pakuwon Jati Tbk Results Presentation

My Stories with PWON

I first purchased PWON shares in 2019 at an initial price of IDR 490 per share. In the same year, PWON reached its historical peak at approximately IDR 810 per share. During the COVID-19 market crash in March 2020, the share price fell sharply to its lowest level, around IDR 200 per share. Despite experiencing a significant floating loss at that time, I chose not to sell my holdings. Unfortunately, I also did not take the opportunity to average down during this period.

Over the years, PWON’s share price has continued to fluctuate, while the company’s financial performance has yet to return to its pre-pandemic peak. In 2019, PWON recorded its highest net profit of IDR 2.720 trillion, largely driven by the office segment. Since the pandemic, revenue from this segment has structurally weakened and has not recovered to its previous level. This reflects a broader shift in demand for office space, influenced by changes in working patterns and corporate real estate strategies.

From a long-term investment perspective, this structural change does not necessarily undermine PWON’s overall business quality. Instead, it highlights the importance of portfolio diversification within the company’s asset base. PWON’s shopping mall and hospitality segments have shown steady recovery and growth, benefiting from the normalization of consumer activity, rising domestic consumption, and the resilience of experiential retail. The segments increasingly serve as the core drivers of recurring income and long-term value creation.

As of the end of 2025, PWON’s share price remains significantly below its 2019 peak. As of 30 December 2025, PWON was trading at IDR 338 per share. For a long-term investor, this valuation gap reflects not only cyclical recovery dynamics but also the market’s reassessment of earnings sustainability and segmental growth prospects. My continued holding of PWON is therefore based on a long-term strategy: focusing on asset quality, recurring cash flow from prime retail properties, and management’s ability to adapt its portfolio to post-pandemic structural shifts, rather than short-term price movements.

At the current stage, I continue to allocate approximately 5.7% of my total investment portfolio to PWON. This position size strikes a balance between conviction and risk management. While I remain cautious about the structural challenges in the office segment, I still view PWON as a long-term holding supported by high-quality retail assets, improving performance in the shopping mall and hospitality segments, and its ability to generate recurring cash flow.

Maintaining a 5–7% allocation allows me to remain invested in the company’s long-term recovery potential while avoiding excessive concentration risk within my portfolio. This position size also provides flexibility to reassess the investment as earnings visibility improves, capital allocation decisions evolve, and broader macroeconomic conditions—such as interest rates and consumer spending—continue to normalize.

This reflects my personal investment decision and perspective. It is not intended as investment advice or a recommendation to buy, sell, or hold any securities. Investing in the capital market involves significant risks, including the potential loss of capital. Each investor should conduct their own research and make decisions according to their individual risk tolerance and financial circumstances.

“The three most important words in investing are margin of safety.”

— Warren Buffett